(Bloomberg Economics) – – With the Covid-19 recession rendering many traditional indicators outdated before they are published, Bloomberg Economics is using a set of high-frequency, alternative data to build daily activity indicators. Here’s what the latest data show:

As expected, economic activity in several of the world’s largest advanced economies plummeted over the Christmas holidays.

An increase in Covid-19 infections and stricter containment measures in November and early December, led activity to drop sharply in the third week of December. A decline in mobility and other alternative data indicators is not unusual over the Christmas and New Year holidays. But in some countries, such as Germany and Italy, very strict containment measures imposed shortly before Christmas added to the weakness.

Japan is the only bright spot among advanced economies. Activity held steady at more than 90% of its pre-virus level both because of a large measure of success in controlling the virus and the lack of the seasonal factor of Christmas.

Our indicators provide a high-frequency guide to the pace of recovery across countries, and attempt to improve the signal-to-noise ratio in alternative data. They are not a substitute for the detailed country view.

The activity indexes are estimated using a dynamic factor model. This methodology extracts an unobservable latent common factor of the underlying high-frequency data in the spirit of Stock and Watson. The model is estimated with daily figures from Jan. 1, 2020 to Dec. 29, 2020.

The high-frequency statistics we use have some obvious advantages — providing a more timely read than traditional data series. They also come with some caveats attached:

The high weight of travel and mobility indicators may lead to overweighting this type of activity in the index.

The index is not fully comparable across countries as we partly use different indicators for different countries, and the relationship between mobility and output likely varies between countries. A complete set of sources is shown in the table below.

We don’t have a long enough time series to map the relationship between the activity indicators and GDP.

In a dynamic factor model, component weights adjust as new data become available. Future updates of the index will likely result in small backward revisions to historical readings.

Our model nowcasts missing data points. That can mean backward revisions of past readings as new data become available.

High-Frequency Indicators Included in Factor Model

Αφήνοντας σιγά σιγά το 2020 και μπαίνοντας στο 2021 είναι σκόπιμο να κάνουμε κάποιες παρατηρήσεις για την ελληνική οικονομία για να κατανοήσουμε που βρισκόμαστε, που πηγαίνουμε με βάση τα στοιχεία του προϋπολογισμού του 2021 και ποιοι θα πρέπει να είναι οι βασικοί στόχοι και κατευθύνσεις.

Του Γιώργου Αναβαλόγλου

Αν και δεν έχουμε τα οριστικά στοιχεία του ΑΕΠ για το 4ο τρίμηνο του 21, αυτό που με λύπη παρατηρούμε είναι ότι η ελληνική οικονομία έκανε το χειρότερο “rebound” σε σχέση με τις υπόλοιπες χώρες της Ε.Ε το τρίτο τρίμηνο του 2020 και βρίσκεται σε επίπεδα ΑΕΠ 1996, όπως βλέπουμε παρακάτω. Ενώ όλα τα κράτη μέλη ακόμη και η Ιταλία σχημάτισαν το λεγόμενο V σχήμα το τρίτο τρίμηνο, στην Ελλάδα δυστυχώς δε συνέβη κάτι τέτοιο:

Αν και η κυβέρνηση προσπάθησε να καλύψει τα λάθη της με τις αναθεωρήσεις του έτους αναφοράς από το 2010 στο 2015, υποστηρίζοντας ότι η ύφεση δεν είχε έρθει πριν την πανδημία (κάτι που οφείλεται στην αλλαγή του έτους αναφοράς και όχι σε αναθεώρηση των στοιχείων του ΑΕΠ), εντούτοις το παραπάνω γράφημα είναι αμείλικτο: στέλνει την ελληνική οικονομία σε επίπεδα στο 1996, διαγράφοντας τα όποια οφέλη είχε από την είσοδο της στο ευρώ.

Αναφορικά τώρα με το μεγάλο θέμα των μέτρων στήριξης της ελληνικής οικονομίας, ενώ η κυβέρνηση ισχυρίζεται ότι έως τέλος του έτους θα δώσει 24 δισ. €, από την εκτέλεση του κρατικού προϋπολογισμού βλέπουμε ότι έως τον Οκτώβριο έχουν γίνει μόλις 6,7 δισ. € κρατικές δαπάνες. Τα υπόλοιπα έως τα 24 δισ. € υπολογίζονται προφανώς από τις αναστολές φόρων, εισφορών κτλ., αλλά δε βοηθούν στην τόνωση της οικονομίας.

Αν δει κάποιος τα στοιχεία των ΜμΕ που επωφελήθηκαν από τα προγράμματα εγγυοδοσίας, θα καταλάβει πόσο απογοητευτικά είναι τα πράγματα για τις επιχειρήσεις αυτές. Χαρακτηριστικό παράδειγμα για το χώρο της εστίασης είναι ότι σε μόλις 16 επιχειρήσεις δόθηκε χρηματοδότηση από τα προγράμματα εγγυοδοσίας της Αναπτυξιακής Τράπεζας επί συνόλου 41.559 επιχειρήσεων και το 1/3 του ποσού αυτού έχει δοθεί σε επιχειρήσεις εστίασης με τζίρο 1-5 εκ. €. Είναι φανερό λοιπόν ότι η πλειονότητα των μικρομεσαίων επιχειρήσεων είναι αποκλεισμένη από κάθε οικονομική βοήθεια από την κυβέρνηση, που μόνο σκοπό έχει τη στήριξη των λίγων μεγάλων επιχειρήσεων φίλα προσκείμενων σε αυτή. Προφανώς κάτι τέτοιο θα οδηγήσει σε κλείσιμο χιλιάδων ΜμΕ και είναι οι κατά την έκθεση Πισσαρίδη επιχειρήσεις ζόμπι, οι οποίες πρέπει να διαγραφούν από το χάρτη δια παντός. Καταλαβαίνει κανείς ότι κανέναν κόμμα της αντιπολίτευσης, πόσο μάλλον ο ΣΥΡΙΖΑ – Προοδευτική Συμμαχία δεν μπορεί να συναινέσει σε τέτοιους είδους πολιτικές, που πετάνε στα σκουπίδια τις χιλιάδες των μικρομεσαίων επιχειρήσεων προς όφελος των λίγων. Καμία συναίνεση στο σχέδιο Πισσαρίδη για το Ταμείο Ανάκαμψης δεν μπορεί να δοθεί όταν ξεχνά έναν από τους βασικότερους κανόνες της Πράσινης Μετάβασης: To leave no one behind, να μη μείνει κανείς πίσω την επόμενη ημερά.

Δυστυχώς η ψήφιση του προϋπολογισμού για το 2021, δε μας αφήνει περιθώρια αισιοδοξίας όταν για παράδειγμα τα μέτρα στήριξης της οικονομίας από τα 24 δισ. του 2020, πέφτουν στα 7,5 δισ. € το 2021. Αν κάνει κανείς τη σύγκριση αναλογικά όπως τα περιγράψαμε πριν, με τα πόσα πραγματικά θα φτάσουν στην οικονομία, καταλαβαίνει ότι η πλειονότητα των εργαζομένων και των επιχειρήσεων θα αφεθούν στο έλεος του Θεού.

Παντού ανά τον πλανήτη υπάρχει το μεγάλο ερώτημα του cliff edge: τι θα γίνει δηλαδή αν τελειώσουν απότομα τα μέτρα στήριξης της εργασίας και τροποτινά βρεθεί ένας μεγάλος αριθμός εργαζομένων χωρίς καμία προστασία, σαν να αφήνεται να πέσει στο γκρεμό. Μέχρι σήμερα είναι γνωστό ότι οι αναστολές συμβάσεων εργασίας θα ισχύσουν ως και τον Ιανουάριο του 21. Δεν υπάρχουν άλλα διαθέσιμα κεφάλαια στον προϋπολογισμό πέραν του Ιανουαρίου. Τι θα γίνει άραγε μετά για τους χιλιάδες (μπορεί να ξεπερνά και το εκατομμύριο) εργαζόμενους; Θα επιστρέψουν ξανά στη δουλειά τους; Θα ξανανοίξουν οι επιχειρήσεις που εργάζονταν σα να μην έχει συμβεί τίποτα; Μέχρι και σήμερα για παράδειγμα δεν υπάρχει καμία ένδειξη για το πότε θα ανοίξει ξανά η εστίαση. Τι θα γίνει με αυτές τις επιχειρήσεις; Η κυβέρνηση λέει θα είναι πάντα δίπλα. Πως ακριβώς και πότε; Αφού έχουν βάλει λουκέτο οι επιχειρήσεις; Λήγουν οι αναστολές πληρωμών φόρων, εισφορών και δόσεων των δανείων στις τράπεζες τον Απρίλιο του 21 και ακόμη δεν έχει αποφασιστεί πως θα πληρωθούν όλα αυτά τα χρέη. Θα υπάρξουν 120 δόσεις; Κανείς δεν ξέρει ακόμη. Και μετά τι; Θα αρχίσει ο κόσμος που έχει μείνει χωρίς δουλειά να πληρώνει το βουνό χρεών που θα έχει μαζευτεί ή θα κοιτάξει τα προς το ζην;

Είδαμε επίσης από τον στρατηγικό σχεδιασμό του ΟΔΔΗΧ ότι οι χρηματοδοτικές ανάγκες τριπλασιάζονται το 2021 σε σχέση με το 2020 (22 δισ. από 7 δισ. €) και ότι για πρώτη φορά μπαίνει τόσο βαθιά το χέρι στο μαξιλάρι (8,7 δισ. €) λόγω της κάλυψης ελλείμματος για το 2021 περί τα 8,1 δισ. €. Καταλαβαίνουμε βέβαια ότι το έλλειμμα μπορεί να αυξηθεί και άρα το χέρι να μπει ακόμη πιο βαθιά στο μαξιλάρι.

Επίσης αν και για το 21 υπάρχει εξαίρεση στους δημοσιονομικούς κανόνες και ευελιξία και αν και η Ελλάδα συμμετέχει τουλάχιστον ως το Μάρτιο του 22 στο PEPP (πρόγραμμα αγοράς ομολόγων της ΕΚΤ), δε βλέπουμε να γίνεται καμία κουβέντα για το τι θα ισχύσει με τα πλεονάσματα από το 2022 και έπειτα. Θα ισχύσει το 3,5% πρωτογενές πλεόνασμα και από το 2023 το 2%+ ; Αν γίνει κάτι τέτοιο θα μιλάμε για την απόλυτη καταστροφή σε μια οικονομία διαλυμένη που έχει επιστρέψει στο 1996. Δεν πρέπει από τώρα να ασκηθούν πιέσεις προς μια κατεύθυνση ίσης μεταχείρισης με τα άλλα κράτη μελη της Ε.Ε λόγω κορονοϊού; Δεν μπορεί να ισχύσει η συμφωνία για το χρέος καθώς μιλάμε για μια νέα οικονομική πραγματικότητα παγκοσμίως που όμως βρίσκει το πιο αδύναμο κράτος της Ε.Ε στη δυσχερέστερη θέση εξαιτίας και της μεγάλης εξάρτησης του από τον τουρισμό, όπου οι απώλειες υπολογίζονται σε πάνω από 15 δισ. € για το 2020.

Εν κατακλείδι, αυτό που θα πρέπει να γίνει το 2021, είναι να παρέμβει η ελληνική κυβέρνηση μέσω νεών ειδικών προγραμμάτων της Αναπτυξιακής Τράπεζας, με τα οποία θα εγγυάται τη συμμετοχή όλων των μικρομεσαίων επιχειρήσεων, καθώς δεν έχουμε την πολυτέλεια να χάσουμε ούτε μία επιχείρηση. Η Αναπτυξιακή Τράπεζα θα πρέπει να ακολουθήσει το μοντέλο λειτουργίας άλλων χωρών όπως της Γερμανίας (KfW) και να βγει μπροστά για τη διάσωση της οικονομίας. Ο χώρος της εργασίας θα πρέπει να στηριχτεί τουλάχιστον για όσο οι επιχειρήσεις μένουν κλειστές.

Το 2021 είναι ίσως το τελευταίο έτος όπου δεν θα τηρηθούν οι δημοσιονομικοί κανόνες και θα πρέπει να το εκμεταλλευτούμε αυτό στηρίζοντας την οικονομία μας με κάθε τρόπο και με κάθε διαθέσιμο χρηματοοικονομικό εργαλείο. Δεν πρέπει να μείνει κανείς πίσω. Αυτός πρέπει να είναι ο μοναδικός μας στόχος.

Some casinos have reopened since the deal was launched in May

Investors pushed back on loan that offered more than 14% yield

(Bloomberg) — Mohegan Gaming & Entertainment has pulled a $100 million leveraged loan sale that was intended to refinance debt and keep its casinos afloat during the pandemic.

The company had offered to pay a yield of over 14% for the new loan maturing in October 2021. The borrower is an extension of the Mohegan tribe in Connecticut and operates the Mohegan Sun in that state as well as other casinos in North America.

“It was pulled because we were able to open earlier than anticipated and have enjoyed very strong operational results,” a spokesperson for the company said in an emailed statement.

A representative for Credit Suisse Group AG, which was leading the loan offering, declined to comment.

The casino business in the U.S. has largely ground to a halt amid the Covid-19 pandemic. But several of Mohegan’s managed properties, including Mohegan Sun in Connecticut and Paragon Casino Resort, recently reopened.

Gaming revenues for the Mohegan Sun from June 1 through to June 14 increased about 10% compared to the same period in the prior year, according to a June 18 filing. Income from operations over the same period since reopening increased about 15% compared to the same time in 2019.

Proceeds from the new loan, along with $42 million of cash on the company’s balance sheet, were intended to repay $138 million outstanding on a $250 million revolving credit facility due October 2021, according to a May 12 reportfrom Moody’s Investors Service. The firm assigned a rating that was seven notches below investment-grade on the debt.

Marketing for the loan began in May, but some investors pushed back on the company’s efforts to borrow on concerns about its ability to raise all the money it needs to repay maturing debt and to fund ambitious planned expansion. Commitments were due on May 11.

The company obtained a waiver on June 11 on its 7.875% bonds due in 2024 for any default that may occur from halted gaming operations due to the outbreak, according to the filing. Those bonds last traded at about 85 cents on the dollar and had fallen to as low as 47.5 cents in April, according to Trace data.

(Bloomberg) — The European Central Bank said it will allow some banks to resume partial dividend payments next year, while urging them to maintain financial reserves to weather the pandemic. For the first nine months of next year, banks should keep dividends and share repurchases to less than 15% of profit for 2020 and 2019 or 0.2% of their key capital ratio, whichever is lower, the ECB said.

European lenders, whose shares have lagged behind the broader market this year, have repeatedly warned that the ECB’s de-facto ban on dividends risks driving investors away. Despite optimism that the end of the pandemic is in sight, some regulators remain concerned that allowing a full return to payouts may leave banks without the financial reserves to bear losses without taxpayer bailouts.

The Bank of England said last week that it will allow lenders to make payouts that don’t exceed 0.2% their risk-weighted assets, or 25% of cumulative quarterly profits over 2019 and 2020 after deducting shareholder distributions. Bloomberg reported last week that European regulators planned to take a more conservative approach than the BOE.

Οι ευρωπαίοι ρυθμιστικοί φορείς των τραπεζών, οι οποίοι πλησίαζαν πιο κοντά στην άρση της de-facto απαγόρευσης των μερισμάτων, ανησυχούν ολοένα και περισσότερο για την επιδείνωση της οικονομικής προοπτικής και τον αντίκτυπό της στους ισολογισμούς των δανειστών λόγω του επανεμφανιζόμενου κοροναϊού.

Καθώς οι τράπεζες πιέζουν τις ρυθμιστικές αρχές να αποκαταστήσουν τη διανομή μερισμάτων, μια συμβιβαστική επιλογή που εξετάζεται από τους αξιωματούχους είναι ότι οι ισχυρότερες τράπεζες μπορούν να πληρώνουν μέρισμα, αλλά να περιορίζουν το ποσό του ετήσιου κέρδους που μπορούν να πληρώσουν, σύμφωνα με άτομα που γνωρίζουν το θέμα. Οι αβέβαιες προοπτικές που προκαλούνται από την πανδημία θα μπορούσαν ακόμη να επηρεάσουν τους αξιωματούχους που συγκεντρώθηκαν στην Ευρωπαϊκή Κεντρική Τράπεζα για την επέκταση της απαγόρευσης, ανέφεραν άνθρωποι που γνωρίζουν το θέμα.

Το εποπτικό συμβούλιο της ΕΚΤ, το οποίο περιλαμβάνει εθνικές ρυθμιστικές αρχές καθώς και αξιωματούχους της ΕΚΤ, παραμένει διχασμένο παρά το γεγονός ότι ορισμένα μέλη άλλαξαν προηγουμένως τη θέση τους στο να υποστηρίξουν την άρση της απαγόρευσης στις αρχές του νέου έτους. Τώρα που έφτασε το δεύτερο κύμα του κοροναϊού, ανησυχούν για την ικανότητα των τραπεζών να αντιμετωπίσουν τις απώλειες και να συνεχίσουν να δανείζουν την πληγείσα οικονομία.

Ενώ ορισμένοι αξιωματούχοι θέλουν να κρατήσουν το αίτημα για αναστολή πληρωμών για τουλάχιστον αρκετούς μήνες περισσότερο, άλλοι θέλουν να επιτρέψουν στις τράπεζες να αποφασίσουν για τις πληρωμές εάν έχουν επαρκή κεφαλαιακή δύναμη. Ένα τρίτο σενάριο περιλαμβάνει τον περιορισμό των τραπεζών να πληρώνουν ένα περιορισμένο ποσοστό ετήσιου κέρδους.

Ένας αυξανόμενος αριθμός δανειστών από τη σκανδιναβική περιοχή έως την Ιβηρική χερσόνησο πιέζει την ΕΚΤ για να δώσει άδεια να συνεχίσει τη διανομή μερισμάτων αφού η απαγόρευση σφυρηλάτησε ήδη τις υποτιμημένες τιμές των μετοχών. Η ΕΚΤ έχει δηλώσει ότι η αναστολή πληρωμών μερισμάτων αποτελεί μέρος της ανταλλαγής με τις δημόσιες αρχές αφού έλαβαν πρωτοφανή κρατική στήριξη και ρυθμιστικές ελαφρύνσεις.

Η ΕΚΤ δήλωσε ότι το αίτημά της έχει διατηρήσει κεφάλαια περίπου 30 δισεκατομμυρίων ευρώ (35,5 δισεκατομμύρια δολάρια) στο τραπεζικό σύστημα.

Εκπρόσωπος της ΕΚΤ δήλωσε ότι «δεν έχει ληφθεί απόφαση για αυτό το θέμα», χωρίς να σχολιάσει περαιτέρω. Η κεντρική τράπεζα δήλωσε ότι θα λάβει απόφαση για μερίσματα τον Δεκέμβριο. Ένας βασικός παράγοντας θα είναι οι οικονομικές προβολές από το προσωπικό της ΕΚΤ που πρόκειται να δημοσιευθούν στις 10 Δεκεμβρίου, ανέφεραν τα άτομα που γνωρίζουν το θέμα. Το Διοικητικό Συμβούλιο πραγματοποιεί μια συνεδρίαση πολιτικής εκείνη την ημέρα, με τους περισσότερους οικονομολόγους να αναμένουν ότι θα προσθέσει περισσότερα νομισματικά κίνητρα για τη στήριξη της σημαίας οικονομίας.

Το βασικό σημείο τώρα είναι πόσο άσχημα θα επηρεάσει το δεύτερο κύμα την οικονομία και εάν οι τράπεζες έχουν επαρκή αποθέματα για να καταπιούν ζημίες από δάνεια χωρίς να χρειάζονται διάσωση. Οι υποστηρικτές των μερισμάτων υποστηρίζουν ότι η απαγόρευση θα μπορούσε να κάνει τους επενδυτές να χάσουν την πίστη τους στις τράπεζες, ενώ όσοι θέλουν να την επεκτείνουν λένε ότι οι μέτοχοι πρέπει να παραμείνουν υπομονετικοί για να προστατεύσουν την επιβίωσή τους.

Το Διοικητικό Συμβούλιο πρέπει ουσιαστικά να εγκρίνει οποιαδήποτε απόφαση του βραχίονα εποπτείας των τραπεζών της ΕΚΤ να επιτρέψει την επανάληψη των πληρωμών μερισμάτων και αυτό θα μπορούσε να είναι ένα ζήτημα. Το πρόγραμμα έκτακτης ανάγκης για αγορά ομολόγων συνδέεται ειδικά με τη διάρκεια της «φάσης κρίσης» της πανδημίας και ορισμένοι αξιωματούχοι ενδέχεται να αντιταχθούν στο να επιτρέψουν πληρωμές σε τράπεζες ενώ η κρίση βρίσκεται ακόμη σε εξέλιξη.

Οι ρυθμιστικές αρχές πρέπει να επεκτείνουν τα όρια στις διανομές κεφαλαίων των τραπεζών για να βοηθήσουν στην προστασία του χρηματοπιστωτικού συστήματος σε περίπτωση που η παγκόσμια οικονομική ανάκαμψη αποδειχθεί αργή, δήλωσε το Διεθνές Νομισματικό Ταμείο σε ένα τμήμα έκθεσης που κυκλοφόρησε την Παρασκευή.

Ο Andrea Enria, ο οποίος είναι επικεφαλής του εποπτικού συμβουλίου, τόνισε ότι η απαγόρευση είναι ένα εξαιρετικό μέτρο για την αντιμετώπιση της επιρροής από την πανδημία και ότι δεν θα γίνει τακτικό εργαλείο για την ΕΚΤ.

«Θα είμαι τόσο χαρούμενος όσο όλοι οι άλλοι όταν μπορούμε να επιστρέψουμε στην τυπική μας πρακτική, δηλαδή να παρέμβουμε και να περιορίσουμε μόνο τη διανομή μερισμάτων για πιο αδύναμες τράπεζες», δήλωσε η Enria σε συνέντευξή της στο Handelsblatt που δημοσιεύθηκε αυτόν τον μήνα. «Πριν όμως καταργήσουμε την απαγόρευση των μερισμάτων, πρέπει να είμαστε πιο ξεκάθαροι για το πού πηγαίνει η οικονομία. Θα πρέπει επίσης να είμαστε σε θέση να προσδιορίσουμε πόσο αξιόπιστος και στιβαρός είναι ο προγραμματισμός κεφαλαίων των τραπεζών και πάλι. “

Event Oct. 22 (Economist Intelligence Unit) — Working-day adjusted industrial output fell by 3.8% year on year in August, a significant acceleration from the 0.2% drop in the previous month. In the first eight months of the year overall, industrial production contracted by 3.9%.

Analysis Industrial output in Greece has fallen in year-on-year terms in 16 of the past 18 months, indicating that the current weakness is not just related to the fallout from Covid-19. However, the pandemic has clearly had a negative impact on both supply and demand in industry, and production collapsed by 10.7% year on year in April and by a further 8.1% in May, two of the months when global supply chains were worst affected.

While this supply shock has been mostly unwound since, the negative demand effect of the pandemic remains significant. Although output was almost flat in year-on-year terms in July, the August data provide a reminder that operating conditions for Greek manufacturers remain extremely challenging.

The brunt of the fallout so far this year has been suffered by consumer durable goods output, which contracted by 11.2% year on year in January-August. Over the same period energy output was down by 6.9% and intermediate goods production by 3.4%.

Output of capital goods and consumer non-durables has held up somewhat better, falling by 1% and 1.3% respectively over the period.

Although the trough of the current downturn is likely to have been in Q2 2020, there are few reasons to think that a swift recovery is on the cards. Latest data from across Europe suggest that a second wave of infections is already under way, and governments in many countries have started to retighten lockdown measures.

This, in turn, will reduce demand for many industrial goods. The latest IHS Markit manufacturing purchasing managers’ index (PMI) for Greece provided, if not grounds for optimism, then at least reason not to be too despondent about near-term prospects for the country’s industry.

The headline reading was 50 in September, exactly on the level separating expansion from contraction but the first reading at or above 50 since February. However, the survey data contained plenty of reasons for caution, not least a further squeeze on firms’ margins and a rising reported level of uncertainty about the near-term economic outlook.

Impact on the forecast Assuming the introduction of tighter public restrictions in the fourth quarter, and taking account of the eight-month data, we will revise down slightly our industrial production estimate of -3.8%

Την Παρασκευή (16.10.20) η ΕΛΣΤΑΤ προχώρησε σε αναθεώρηση του ΑΕΠ των προηγούμενων ετών (2010-20170 και ο κύριος Σταϊκούρας άσκησε κριτική στο ΣΥΡΙΖΑ, γιατί τελικά όπως προκύπτει με τα νέα στοιχεία, η αύξηση του ΑΕΠ μας ήταν μικρότερη του μέσου όρου της Ευρωζώνης. Μάλιστα είπε ότι παρέδωσε ανάπτυξη η ΝΔ το 2014 και ο ΣΥΡΙΖΑ το γύρισε σε ύφεση παραθέτοντας τον παρακάτω πίνακα:

Αυτό που δεν είπε όμως είναι ο λόγος που έγινε αυτή η αναθεώρηση , ο οποίος είναι η αλλαγή του έτους ΒΑΣΗΣ που υπολογίζεται το ΑΕΠ της χώρας, το οποίο άλλαξε από το 2010 που ήταν στο 2015. Άρα δεν πρόκειται για μια αναθεώρηση ΑΕΠ που γίνεται π.χ ανά τρίμηνο, αλλά λόγω της αλλαγής του έτους αναφοράς, κάτι που συμβαίνει ανά 5ετια. Επιπλέον:

Eίπε ο κος Σταϊκούρας ότι ο ΣΥΡΙΖΑ παρέλαβε ανάπτυξη από τη ΝΔ. Για να δούμε λοιπόν τι ανακοίνωσε η ΕΛΣΤΑΤ γιατί προφανώς για τη ΝΔ δεν υπήρξε οικονομία πριν το 2014. Όπως φαίνεται στο γράφημα της ΕΛΣΤΑΤ, τα στοιχεία για το ΑΕΠ είναι : -10,1% το 2011, -7,1% το 2012, -2,7% το 2013 και 0,7% το 2014

Καυχιούνται δηλαδή για μία αύξηση του ΑΕΠ 0,7% μετά από μια σωρευτική πτώση του ΑΕΠ 19,9%. Για να τελειώνουμε με τα αστεία η ελληνική οικονομία βρίσκετε αυτή τη στιγμή σε επίπεδα ΑΕΠ 1997 με αποπληθωρισμό 2% ο οποίος είναι και ο χειρότερος στην ευρωζώνη και να τονίσουμε ότι είναι και ο χειρότερος εφιάλτης της ΕΚΤ :

Παράλληλα όμως με την ανάπτυξη 0,7% η Νέα Δημοκρατία παρέδωσε το 2014 και ένα έλλειμμα 3,6%; Για να δούμε και πόσο ήταν αυτό και τα προηγούμενα χρόνια;

Επίσης ξεχνάει η ΝΔ τη παγίδα χρέους που είχε στήσει με αυτήν την καταπληκτική ρύθμιση του μέσω του PSI. Πως θα γινόταν αποπληρωμή χρέους 28,3δις € μόνο για το 2015, με άδεια ταμεία και όντας αποκλεισμένοι από τις αγορές;

Τέλος υπάρχει και η πρόσφατη ανάλυση του Economist, που αναφέρει ότι η ύφεση στην Ελλάδα είχε έρθει πολύ πριν την πανδημία, λόγω των δύο συνεχόμενων αρνητικών τριμήνων (4ο του 2019 και πρώτο του 2020), το οποίο είναι ο ορισμός της τεχνικής ύφεσης.

Καλό είναι λοιπόν ο κύριος Σταϊκούρας αντί να χάνει χρόνο προσπαθώντας να δημιουργήσει εντυπώσεις για το αν τα πήγε συγκριτικά καλύτερα ο ΣΥΡΙΖΑ τα προηγούμενα χρόνια όπου είχαμε ανάπτυξη, σε σχέση με την υπόλοιπη Ευρωζώνη, να συνειδητοποιήσει πόσα χρόνια πίσω έχει γυρίσει η χώρα μας και τι μπορεί να κάνει για να στηρίξει την οικονομία.

Ένα είναι σίγουρο. Το να αρπάζει την περιουσία και το εισόδημα του ελληνικού λαού μετά από μνημόνια και εν μέσω πανδημίας δεν είναι λύση. Εκτός και αν το μόνο που έχει στο μυαλό της η Νέα Δημοκρατία είναι να εξυπηρετεί τις τράπεζες και τα funds.

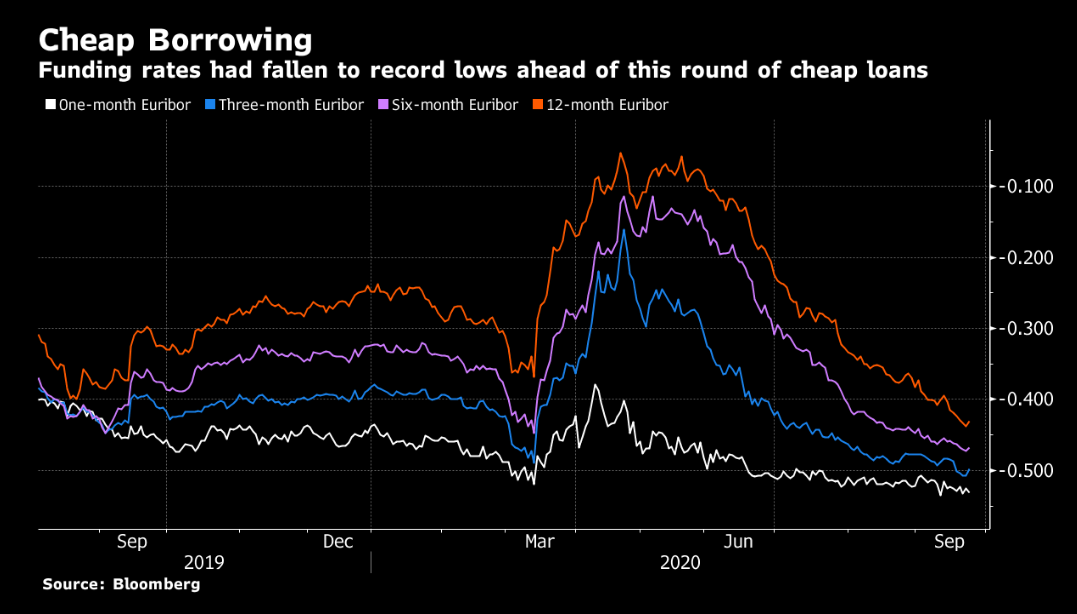

The takeup may lift excess liquidity to 3 trillion euros

Central bank facility is designed to encourage banks to lend

(Bloomberg) —

Euro-zone banks took 174.5 billion euros ($203 billion) in another dose of ultra-cheap funding as the European Central Bank gives them every possible incentive to keep lending to the pandemic-stricken economy.

The bids for the targeted loans, known as TLTROs, came from 388 banks, and the takeup was at the high end of economists’ expectations. The loans will likely push excess liquidity in the euro zone above 3 trillion euros for the first time on record. The euro fell as much as 0.2% to $1.1633.

“This should weigh on Euribor fixings in the coming days,” said Rishi Mishra, an analyst at Futures First. “The fact that banks are willing to borrow more is an unequivocally positive outcome, as it means monetary policy is alive and kicking in more ways than just QE and forward guidance.”

The takeup, while high, was well below the record 1.3 trillion euros in the previous round three months ago, suggesting that most lenders now consider themselves well-financed.

The three-year loans have become one of the ECB’s most-important tools during the coronavirus crisis. They carry an interest rate as low as minus 1% — meaning the ECB pays banks to borrow — as long as they are used to fund credit to companies and households.

They also more than compensate banks for the official policy rate of minus 0.5%, which works as a charge on their reserves and erodes their profitability. Without TLTROs as a counterbalance, that could eventually curb lending.

Piet Christiansen, chief strategist at Danske Bank A/S in Copenhagen, estimates that excess liquidity will rise by another 600 billion euros to 800 billion euros by the summer of 2021.

Dual-Rate System

Some economists reckon the ECB has stumbled on a dual-rate system that allows it to cut borrowing costs with no practical limit without damaging the banking system.

Still, the extraordinary access to cheap cash — combined with other monetary stimulus such as massive bond-buying programs — does raise the prospect of side effects such as elevated asset prices and risky lending.

It could even undermine the ECB’s influence over short-term market rates. Three-month Euribor — the rate at which banks can theoretically borrow from one another — fell to a record low of minus 0.508% this week.

When it dropped below the ECB’s policy rate last week, that was a phenomenon that had happened only once before, in August 2019, shortly before the central bank cut its deposit rate. Euribor futures, which reflect the three-month benchmark rate held small gains following the announcement, a sign borrowing costs may fall further.

More stimulus could be ahead. The ECB projects that the economy will contract 8% this year, and the inflation rate has fallen below zero for the first time in four years. Rising coronavirus infections could worsen the outlook.

Economists predict the 1.35 trillion-euro pandemic bond-buying program will be expanded again this year. Markets aren’t pricing another 10 basis-point rate cut until October 2021.

“We think this dovish view should and will prevail,” said Frederik Ducrozet, chief global strategist at Banque Pictet & Cie in Geneva.

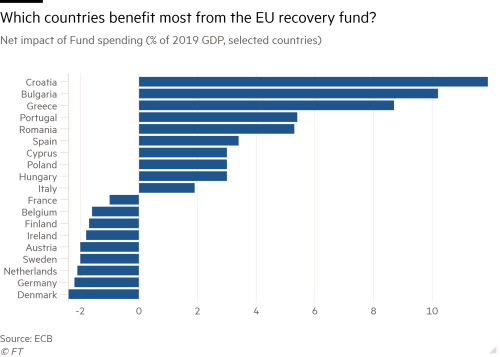

The European Central Bank has urged the EU to consider making its new pandemic recovery fund permanent, as it published data showing that Croatia, Bulgaria and Greece would be the fund’s biggest net beneficiaries.

The EU plans to issue €750bn of debt to support a revival of the region’s pandemic-stricken economy by distributing grants and loans to member states, a move the ECB called “an important milestone in European economic policy integration”.

The scheme’s centrepiece — €390bn of grants — would provide a net benefit worth more than 10 per cent of the pre-crisis Croatian and Bulgarian economies and almost 9 per cent for Greece, the ECB estimated in a research note published on Wednesday.

Also among the net beneficiaries are Portugal, which will gain 5.4 per cent of its 2019 GDP; Spain with a gain of 3.4 per cent of GDP, and Italy with a gain of 1.9 per cent of GDP.

The scheme “ensures stronger macroeconomic support for more vulnerable countries”, the ECB said.

The heaviest net losers include the “frugal four” countries that initially opposed the new fund. Austria, Denmark, Sweden and the Netherlands will all lose out on a net basis by nearly 2 per cent of pre-pandemic GDP, as will Germany, according to the central bank’s analysis.

The ECB assessed the benefit each country would derive from the grants after deducting the cost of repaying its share of the extra EU debt needed to fund them.

It noted that although the fund is “a one-off” it “could also imply lessons for economic and monetary union, which still lacks a permanent fiscal capacity at supranational level for macroeconomic stabilisation in deep crises”.

The EU should consider making the fund a more permanent part of its policymaking arsenal when it restarts talks on its budget rules, the ECB said.

The finance raised by the fund will increase the EU’s outstanding debt 15-fold, the ECB estimated.

ECB officials have long argued that the EU should issue a large, commonly guaranteed pool of debt to rival German Bunds in a bid to reduce the bloc’s vulnerability to future national sovereign debt crises.

However, the idea is contentious among conservative policymakers who insist the recovery fund — dubbed Next Generation EU — should only be a temporary crisis-fighting tool and worry that some countries may not make efforts to repay EU loans.

Jens Weidmann, president of Germany’s central bank, warned this month about the risk of “creating the impression that debt at the EU level somehow doesn’t count or that it is a way of evading tiresome fiscal rules”. He added that the recovery fund should “remain a clearly defined crisis measure and should not open the door to permanent EU debt”.

But the ECB said: “Provided it is deployed for productive spending and accompanied by growth-enhancing reforms, Next Generation EU would not only help to underpin the recovery but also increase the resilience and growth potential of member state economies.”

It estimated that the overall financial support from the fund would be equal to almost 5 per cent of eurozone gross domestic product.

Economists worry about the longer term financial sustainability of some southern European countries that are expected to vastly increase their budget deficits to fund their response to the coronavirus pandemic. Greece’s debt is expected to rise above 200 per cent of GDP, while Italy is set to exceed 160 per cent and Spain is heading towards 130 per cent.

Fabio Panetta, an ECB executive board member, said in a speech on Tuesday that for heavily indebted countries “the sizeable funding provided at the European level presents a unique opportunity to address concerns of competitiveness and long-term sustainability”.

He added: “Growth will be the only solution to the accumulation of public and private debt.”

The European Central Bank has launched a sweeping review of its main pandemic crisis-fighting tool, which some of its top policymakers believe could lead to contentious changes to its other asset-purchase programmes.

The review will assess the impact of the flagship bond-buying scheme that the ECB launched in response to the coronavirus crisis in March and expanded to €1.35tn in June, two of its governing council members told the Financial Times on condition of anonymity.

They said important questions for the review would be to consider how long the Pandemic Emergency Purchase Programme should continue and whether some of its extra flexibility should be transferred to the ECB’s longer running asset-purchase schemes.

“Having that extra flexibility has been very useful,” said one council member. “We should look at all bits of the toolkit very carefully. We will have a good discussion, a good debate, and I don’t know where we will end up.”

The ECB declined to comment on the review, which is expected to be discussed by the council next month. It comes as debate is intensifying on the council over whether it should start drawing up plans to wind down the PEPP or consider expanding it further.

Until the new programme’s introduction, the ECB’s sovereign bond purchases were bound by self-imposed rules, designed to avoid it being accused of using monetary policy to directly finance governments, which is illegal under EU law.

It might be easier for some national central banks to accept that we expand the traditional asset purchase programme rather than the PEPP

ECB council member This changed with the PEPP, which ditched the restriction of only buying up to a third of a country’s debt and introduced a more flexible interpretation of the rule requiring it to buy sovereign bonds in proportion to the size of each country’s economy.

It also started buying Greek government bonds, breaking with the ECB’s tradition of not buying debt rated below investment grade.

Any move to increase the flexibility of the ECB’s overall bond-buying programme is likely to prove controversial, particularly among its critics in Germany who are gearing up to launch another legal challenge at the country’s constitutional court.

When the court ruled in May that the ECB needed to do more to explain why its government bond-buying had not breached EU law, it pointed to the self-imposed rules as a key reason why the purchases still appeared to be legal.

A second council member said the review would look at whether the ECB should shift away from using the PEPP and focus instead on increasing the scale of its other asset purchase programmes, while potentially giving them the same extra flexibility.

“It might be easier for some national central banks to accept that we expand the traditional asset purchase programme rather than the PEPP,” said the second council member.

Some ECB council members are concerned that the PEPP risks becoming a more lasting part of the central bank’s policy framework, especially after it was extended from the end of this year until June 2021.

Jens Weidmann, president of Germany’s Bundesbank and one of the longest-serving ECB council members said this month that “the emergency monetary policy measures must be scaled back when the crisis is over”. He added: “When deciding on the PEPP, it was particularly important to me that it have a time limit and be explicitly tied to the crisis.”

As of last week, the ECB had bought €527bn assets under the PEPP on top of the more than €2.8tn of assets it owns under its other asset purchase programmes. Some economists expect it to increase its bond-buying plans by a further €500bn as early as December in an attempt to raise inflation back towards its target of just below 2 per cent.