Hurt by worries about global growth, the S&P 500 on Monday fell as much as 1.89 percent before reversing course and ending the session with a 0.17 percent gain, trimming its loss so far in December to 4.44 percent.

The S&P 500 index has been in a correction since October, defined by many investors as a drop of 10 percent or more from a high. It has not crossed the 20 percent threshold, widely viewed as the definition of a bear market.

However, 245 stocks in the S&P 500 – 49 percent of its components – on Monday had fallen 20 percent or more from their 52-week highs. Another 127 S&P 500 stocks had fallen 10 percent or more from their 52-week highs, but less than 20 percent.

(Graphic: Half of S&P 500 stocks in bear market – tmsnrt.rs/2zOJImb)

The index on Monday was down about 11 percent from its Sept. 20 record high close.

Apple Inc (AAPL.O), until recently Wall Street’s most valuable company and the largest component of the S&P 500, has declined 27 percent from its record high on Oct. 3, accelerating the index’s losses as investors fret over cooling demand for iPhones.

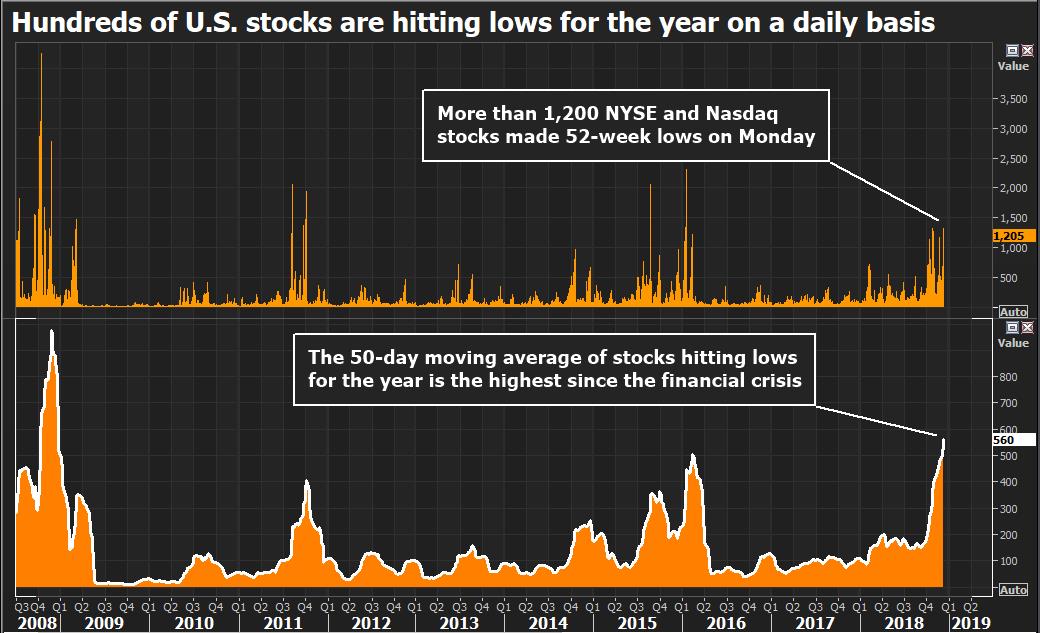

Pessimism has spread beyond the S&P 500 to smaller companies across the U.S. stock market, with hundreds of stocks hitting lows for the year on a daily basis in recent sessions.

(Graphic: Stocks hitting 52-week lows – tmsnrt.rs/2SBWw6w)

S&P 500 components deepest in bear market territory include Nektar Therapeutics (NKTR.O), Coty Inc (COTY.N) and General Electric Co (GE.N), each down more than 60 percent from its 52-week high.

Microsoft Corp (MSFT.O), which in late November dethroned Apple as Wall Street’s largest company, is down 8 percent from its Oct. 3 record high.